SBI returned money to bondholders who put their money in 15 years bond in SBI Retail bond in March 2011 with 9.95% annually have got their investments back ahead of maturity.

With the interest rate going down it was natural for SBI to call their bonds in 10th year, when five year Fixed deposit rates were 5.4% annually. Retail investors and retirees were the major holders of this bonds as they come from government backed entity.

There are various others investments options who have got their money back like Index Fund/ETFs with return of 10%-14% compounded annually.

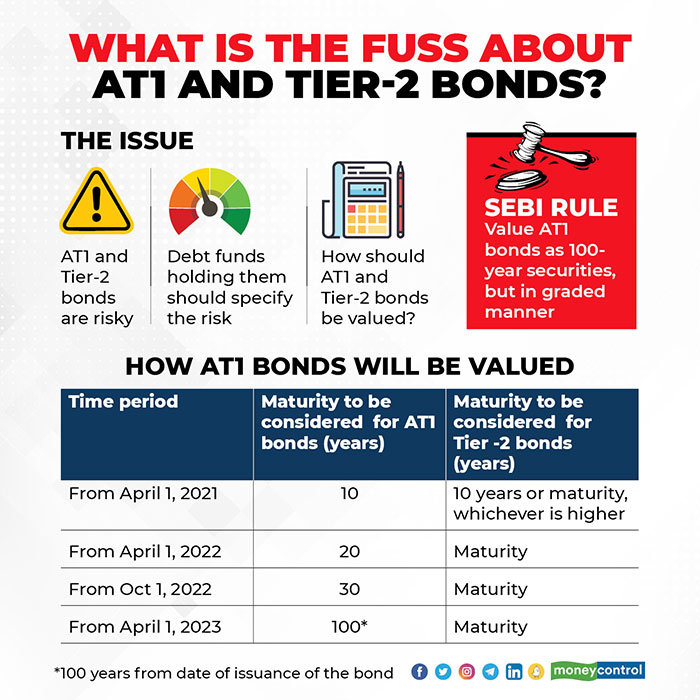

The Securities and Exchange Board of India (SEBI) on 10th March,2021 asked mutual funds to value perpetual bonds as 100-year instruments from April 1. While the SEBI circular under discussion, it attempts to address the issue of using perpetual bonds inappropriately in MF schemes . This new valuation norm is expected to spark a sharp selloff of these bonds. Due to the change in valuation norms present value of perpetual bonds on the books of mutual funds will fall. Bond yields and prices move in opposite directions. Additional Tier 1 and Tier 2 bonds (AT1 and AT2) are such bonds. Mutual funds are one of the largest investors in perpetual debt investments and currently hold Rs35,000 crore of the outstanding AT-1 issuances of about Rs90,000 crore. These are perpetual bonds i.e., these bonds have no maturity. Thus, the banks do not even have to pay back the principal if they wish. They can just keep paying the periodic interest. And the claims of such bondholders can be subordinate to equity investors. Hence, unlike other bonds, these AT1 and AT2 bonds are much riskier bonds When debt funds invest in a security, they expect to earn an interest income throughout the instrument’s tenure. The principal amount is paid at maturity. If the organisation goes bankrupt or gets into financial trouble, priority must be given to debt funds in paying the dues. But not all instruments are at the same priority level when the borrowing firm needs to repay its creditors. Holders of AT1 bonds come last in the queue after bank depositors, general and other creditors in the payment of dues if the firm goes bankrupt. There have also been cases where AT1 bonds have been completely written-off by the bank, under directions of Reserve Bank of India. In the case of Yes Bank, RBI wrote down the AT1 Bonds to zero (equity was not written down to zero), resulting in a total loss to AT1 bondholders. In case of Laxmi Vilas Bank, both equity and AT2 bonds were written down to zero. Accelerated redemptions in debt schemes could trigger a crisis as mutual funds are dumping such securities, causing yields to spike and making it costlier for banks to borrow funds from the market. Accordingly, the MF portfolio will calculate its NAV. Now, as per the new SEBI rule, the same bond must be valued as if it is maturing in 100 years. As we don’t have a benchmark for a 100-year bond yet. However, we know that long duration bonds usually trade at higher yields than short duration bonds because when you lend for less than a year, you are almost sure that nothing will go wrong in a year and you will get your money back. The same can’t be said if you are lending for 100 years. Things can go wrong. And you must be compensated for higher risk. That’s why investors demand higher yields (or interest rate/coupon) for longer maturity bonds. And this can affect valuation of such perpetual bonds in debt mutual fund portfolios. How?. Let us consider an example, A Mutual Fund scheme has invested in a Two perpetual bonds (Bond A and Bond B). The bond A is callable in 5 years and bond B is callable in 100 years. Now, the AMC will price it as if the bond A and bond B maturing in 5 years and 100 years respectively. Both perpetual bond pays a coupon of 7% p.a. Assume the prevailing 5 years bond yield is 6.55% and 100 years bond yield is 8.75% (we need to add a significant risk premium). In that case, bond A will be priced at ₹ 101.86 and bond B will be price at ₹ 80 by the method of Present value of future cash flows.

Years Coupon YTM FV PV Bond A. 5. 7%. 6.55%. ₹ 100. ₹ 101.8

Bond B. 100. 7%. 8.75%. ₹ 100. ₹ 80

As the number of years increases the YTM of bond also increases and price decreases. That’s an almost (-21.46%) cut from price Between Bond A to Bond B. However, one thing is clear. There can be a significant price erosion on values of some of these bonds due to change in valuation norms. And Finally the impact of this New Rules, If your debt MF scheme has 5% exposure to such a bond, the impact will be minimal. Even the price of such a bond is cut by 25%, the impact on MF scheme NAV is only 1.25%. Negligible. Expectedly, some of the banking & PSU debt funds have significant exposure to such bonds. So, if your scheme has 30% exposure to such bonds and the value of such bonds is written off by 25%, the NAV of the MF scheme will go down by 7.5%. That is a big hit to a debt mutual fund scheme. Now, if you know that the NAV of your scheme will go down by 7.5% on April 1, 2021, you might consider exiting this investment. As more investors, the allocation to perpetual bonds will increasingly become a higher percentage of residual portfolio. More investors will therefore want to exit the fund. AMCs know that. Thus, they might try to sell off the perpetual bonds from their portfolios to contain the damage. But the portfolios won’t be out until the second week of April. So, investors are in the dark about the actions the AMCs are taking. Whole lot of confusion. Lastly, if the exposure to AT1 bonds in your scheme is high and there is no clawback (or extension) of 100-year rule, you might want to reconsider your investment in the MF scheme. The finance ministry dated 11th March 2021 to the chairman of the Securities and Exchange Board of India (SEBI) has asked the markets regulator to withdraw a rule that sought to treat banks’ additional tier 1 (AT1) bonds as having 100-year maturity, making investments in them one of the riskiest, as the government feared a sell-off in these securities would make it tougher for banks to raise capital. In general, after what happened with Yes Bank AT1 bondholders, you should avoid schemes with heavy exposure to AT1 bonds, especially from weaker banks. However, The Securities and Exchange Board of India (SEBI) issued a circular on 22nd March 2021, postponing the 100-year maturity rule for valuing perpetual bonds by two years.